Justine and Olivia Moore, known in the capitalization industry as the Venture Twins (they are twin sisters who attended Stanford together and now work together at venture capital firm CRV, which has Patreon in its portfolio), sometimes train their lens on podcasting. Following Spotify’s recent cage-rattling acquisitions of Gimlet, Anchor, and Parcast, the Moores analyzed how venture funding and exit money are balanced between tech companies and content companies in podcasting.

Justine and Olivia Moore, known in the capitalization industry as the Venture Twins (they are twin sisters who attended Stanford together and now work together at venture capital firm CRV, which has Patreon in its portfolio), sometimes train their lens on podcasting. Following Spotify’s recent cage-rattling acquisitions of Gimlet, Anchor, and Parcast, the Moores analyzed how venture funding and exit money are balanced between tech companies and content companies in podcasting.

“As venture investors, we’ve struggled to reconcile the explosive consumer interest in podcasts with lagging revenue and exits, but it looks like this may finally be changing,” they write. The authors take an interest in the exits (in venture terms: acquisitions). “It’s been particularly surprising for us to see content studios, like Gimlet, Parcast, and HowStuffWorks, driving the exit activity.”

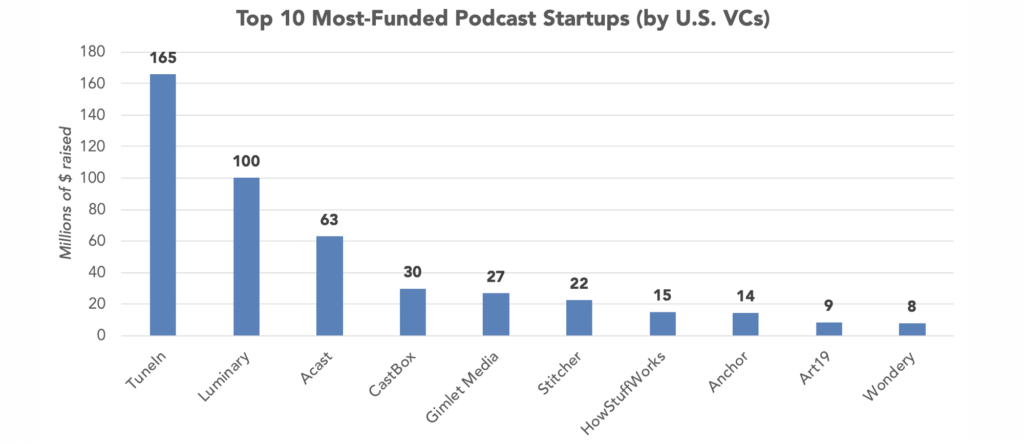

Of interest in the article is that although most podcast venture capital has flowed to tech companies (e.g. podcast hosting, analytics, and distribution platforms), most of the exit money, which traditionally reward investment, has been steered to content companies (show creators and networks). To illustrate, the Twins start by charting the top 10 venture-backed podcast startups:

Most of the investment money is piled into tech — $327M vs. $125M), and that includes Luminary which can go both ways, and is counted as a content company above. If Luminary is flipped into the tech category, content companies in the above chart total only $55M investment.

Most of the investment money is piled into tech — $327M vs. $125M), and that includes Luminary which can go both ways, and is counted as a content company above. If Luminary is flipped into the tech category, content companies in the above chart total only $55M investment.

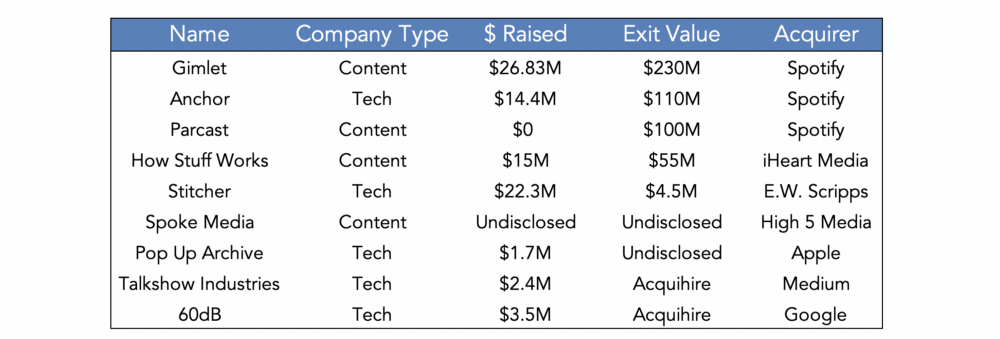

To counterpoint this, Justine and Olivia have a table of exit values representing acquired podcast companies:

The scorecard for exit money is: $385M for content vs. $114.5M for tech. We asked Justine and Olivia Moore why Stitcher (Scripps), PodcastOne (partial acquisition by Hubbard Radio) and Cadence13 (partial acquisition by Entercom) were not represented — the answer is that they were not venture backed. “We focused on exits for VC-backed startups, which we pulled from Pitchbook,” the Twins told us. At any rate, they would have further proved the article’s thesis, since PodcastOne and Cadence13 are content companies; Stitcher is mostly tech.

So, why is this? The analysis is lengthy and worth reading (HERE). One interesting point is that big audio acquirers (think Spotify and iHeartRadio, which acquired Stuff Media) already have tech solution baked into their infrastructures; they seek content to diversify their listener acquisition and retention. In the cases of those two high-profile companies, the article notes, podcasting represents potentially higher margins than the low-margin, high-cost music streaming business. “Spotify can keep 100% of the ad revenue generated against this content,” the Twins note. “Spotify is heavily incentivized to get users to spend more time listening to podcasts, as it’s their highest margin content.

The article predicts that other “share of ear” competitors will move into the acquisition space for podcast content — Pandora, Deezer, Tidal.