The role and value of free listening to on-demand services has been under scrutiny for months. The main focus is Spotify, which uses the freemium model as both a stand-alone service, and to funnel users into paid subscriptions where enhanced features are unlocked. That strategy is controversial, at least reportedly in the context of Spotify’s label negotiations, where rights-owners dislike unpaid listening generally, especially when the on-demand features enable listeners to pick and choose what they hear.

Starting in December, 2013, when Spotify opened up its Spotify Free program to mobile devices, users have enjoyed a fair amount of interactivity outside of the subscription plan. They can call up an individual artist and listen to an auto-shuffled stream of the artist’s discography. They cannot download the music for offline listening, but in an increasingly always-connected world, the download loses meaning for some people.

Label logic says that users must pay for selective listening. That’s what CD’s, downloads, and online music subscriptions are for. It’s understandable that Spotify’s label partners would wish to minimize Spotify Free usage, and maximize Spotify Premium sign-ups.

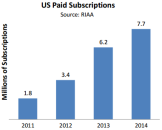

Is there economic justification for label logic? In the RIAA’s report of the 2014 recorded music industry, three types of streaming revenue are broken out:

- SoundExchange distributions to labels (Internet radio, the largest of which is Pandora): $773-million, +31%

- Paid Subscription (e.g. Spotify Premium, Rhapsody, Deezer, Rdio, Beats Music): $799-million +29%

- On-Demand Streaming (this is freemium, e.g. Spotify Free, Deezer’s free plan, Rdio’s free plan): $294-million +34%

So, “label logic” is justified to that extent. But there are other questions of logic.

At a glance, it might seem like Spotify’s 25% sign-up rate is anemic, and that the freemium funnel isn’t working well. But no other subscription service has claimed nearly as many subscribers. In fact, Spotify seems to be the champ at creating a new music-subscription market. when you consider that Spotify also offers the most interactive features of any freemium plan (that’s why it’s controversial, and a reported pivot point in label negotiations), logic seems to say that whatever Spotify is doing, works.

The last 15 years have demonstrated one thing: subscribing to an online music service remains a strange and unpopular concept, at least in the American market. Rhapsody was the first such service to launch here, in 2001, and today has about three-million users. rhapsody is pay-only, no freemium, just like Beats Music (soon to be relaunched by Apple). Music subscription was scorned in the U.S. until 2011, when Spotify crossed the ocean and gave the U.S. market its first free on-ramp to a celestial jukebox. Freemium doesn’t deliver all the pleasure or value of full subscription, but it does introduce enough of the experience to open eyes, change minds, and motivate payment. Many of my acquaintances, who gave me blank, implacable stares when I advocated Rhapsody, are now happy Spotify subscribers.

There’s another point, often forgotten in this discussion. Ad-supported freemium is a stand-alone business, not yet with the high margins of subscription service, but that is a maturation issue. While Pandora, which is really in a different legal and strategic category from Spotify (more about that in another article) is respected as a deeply resourced advertising company, Spotify is almost never acknowledged that way.

Yet quietly, Spotify has been staking ground in the streaming audio advertising market, developing geo-located audience segments, joining Triton Digital’s streaming ratings ranker, and marketing its inventory in Mediaocean, one of the top media advertising market platforms. With these moves Spotify competes against Pandora for advertiser share in the radio market, while the Premium plan competes with iTunes for purchasing share in the music market.

With all this, and considering that streaming music is buttressing the music industry against overall decline (see this), patience and persistence are needed to develop greater scale in all streaming models. Freemium works. Maybe it can be tweaked and optimized. But in a stubborn, resistant market, freemium has demonstrated its power to move people to consider new music-payment choices. At the same time, freemium is maturing as its own scalable business.